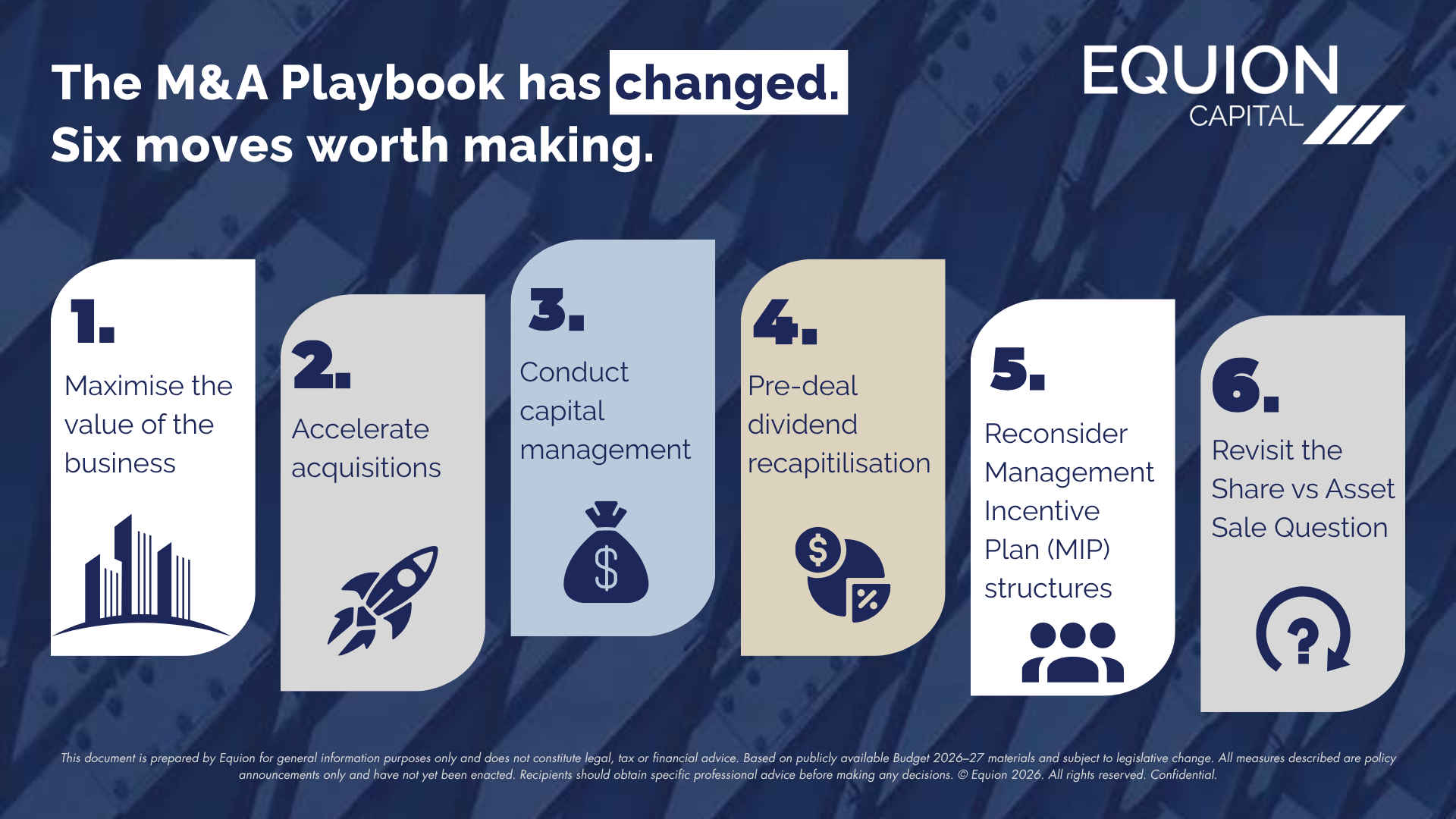

The M&A Playbook has changed. Six moves worth making.

Equion’s view on the Federal Budget 2026-27 and what it means for business owners, founders and sponsors.

Most Budget commentary is either technical to act on or too generic to be useful. What follows are the measures we think matter most, why they matter, and the actions worth considering now.

These initiatives are based on the Budget as proposed. Budget measures must pass through a parliamentary process before becoming law, and the final legislation may differ from what has been announced. We recommend obtaining advice before executing on any plan.

1. Maximise the value of the business

Relevant to: All private business owners and financial sponsors

What we recommend

Commission a strategic review now. There is still time to identify and action the initiatives that move business value before 1 July 2027, following the same process we would apply ahead of a sale. If an exit is on the table, launch by September 2026.

Our view

The 1 July 2027 valuation is a permanently consequential tax event. Gains established on that date stay inside the old regime. Everything above it does not. A higher independently supported valuation on that date is the most powerful lever available.

Engage an independent valuer with genuine fluency in the applicable CGT framework. The ATO’s transitional formula remains unpublished. The gap between a supported market valuation and the ATO default is likely to be material. The right professional draws on comparable transactions, earnings multiples and discounted cash flow in combination, and can defend the number.

For financial sponsors, ‘carry’ accruing on high-growth operating businesses should be approached with the same urgency. Where a full exit is not achievable in time, a continuation fund with an anchor investor offers a credible alternative: market-determined valuation, cost base reset, and a well-established structure.

How Equion can support

We run strategic reviews with owners, assessing the business through the lens of a buyer, a valuer and an adviser simultaneously. We work with specialist valuers, tax counsel and legal partners, coordinated from the outset so the right expertise is in place before it is needed.

2. Accelerate acquisitions

Relevant to: Acquisitive platforms and financial sponsors

What we recommend

Deals already on the agenda, including vertical integration, capability, IP and geographic entry, should be moved forward. Complete and consolidate before the 1 July 2027 reset.

Our view

Acquire and consolidate before the reset and the multiple arbitrage (the difference between acquisition cost and platform value) is locked into the new cost base at 30 June 2027. Acquire after and that same gain sits above the cost base under indexation, where it is not inflation-protected, due to the immediate uplift .

How Equion can support

We run Programmatic Buyside, an outsourced corporate development function for platforms and sponsors with acquisitions to accelerate. Deal sourcing, engagement, structuring and closing, alongside your team. Capacity to transact should not be the constraint.

3. Conduct capital management

Relevant to: Discretionary trust shareholders

What we recommend

Structure and execute shareholder buybacks and dividend streaming strategies before 1 July 2027, while the ability to distribute through a corporate beneficiary remains viable. The earlier this starts, the more options remain possible.

Our view

Corporate Beneficiaries (“Bucket Companies”) lose their structural advantage permanently. Income splitting to lower-rate beneficiaries no longer reduces tax below the proposed 30% floor. For private groups built around trust-and-bucket-company structures, the cost of retaining earnings rises materially from 1 July 2028.

A number of capital management options close permanently once those dates pass. The ones that remain will be fewer and more constrained.

How Equion can support

We model optimal capital structures and assess buyback strategies, whether the objective is facilitating shareholder exits, funding liquidity needs, or returning capital ahead of both trigger dates. We work alongside your tax and legal advisers from the start, so the sequencing is right and the engagement is coordinated.

4. Pre-Deal dividend recapitalisation

Relevant to: Private business owners selling after 1 July 2027

What we recommend

Model a dividend recapitalisation plan before going to market, not during the process. Introduce debt, distribute retained earnings as a franked dividend, and reduce the equity value of the business ahead of a sale. You capture value through franking credits; the buyer acquires a lower equity value; the overall capital gain is smaller. The analysis is worth running well before signing, not at it.

Our view

Under indexation, distributing excess cash as a franked dividend is likely to deliver better after-tax proceeds than retaining it inside the equity value and paying CGT on exit, particularly in a high capital growth business.

Franking account balances, debt capacity and the impact on headline price and due diligence all need to be assessed. The structure that works has to be stress-tested against the transaction, not just the tax.

How Equion can support

We model the recapitalisation alongside the M&A process, working with tax counsel to assess the numbers across multiple scenarios. When built into sale preparation from the outset, the process is typically straightforward. When left until signing, it rarely is.

5. Reconsider Management Incentive Plan (MIP) structures

Relevant to: Private businesses and financial sponsors with management incentive plans

What we recommend

For existing arrangements, consider maximising the 1 July 2027 valuation to establish the highest possible cost base. For new arrangements post-2027, consider moving to a matched co-investment structure with a gross-up transaction bonus, a potentially cleaner alternative to the loan-funded share plan under the new regime.

Our view

The most common structure the loan-funded share plan has underpinned management equity in Australia for twenty-five years, delivering an effective rate of approximately 23.5% on the gain (assuming a 47% marginal tax rate). From 1 July 2027, particularly where capital growth is materially higher than inflation, the new indexation method may produce a worse outcome than the existing 50% discount.

Under a matched co-investment plan, the executive invests in real shares alongside a shadow equity entitlement of equivalent value to the loan funded shares. At exit, the shadow entitlement pays out as a transaction bonus, grossed up for the tax shield. The net cost to the buyer, after the tax shield deduction, is structured to approximate the pre-gross-up entitlement. No company loan. Broadly self-funding in a well-structured transaction.

How Equion can support

We review existing MIP structures and model alternatives ahead of the 1 July 2027 deadline. We position the gross-up mechanics in the Information Memorandum and with buyers throughout the process, so the tax shield on transaction bonuses is recovered, not left on the table. We then work with your tax and legal advisers to embed the co-investment structure, or shadow equity entitlement, into both the management documentation and the transaction documents.

The window is thirteen months. Transaction activity, independent valuations and regulatory filings will all increase materially as 1 July 2027 approaches. The businesses that prepare early will be ahead of the queue. Those that wait until late 2026 will be competing for scarce capacity against a deadline that cannot move.

6. Revisit the Share vs Asset sale question

Relevant to: Private business owners selling after 1 July 2027

What we recommend

Before designing a sale process around a share sale, run the numbers on an asset deal. For most businesses under the old regime, the share sale was often preferably from a tax perspective, but also simplicity. That may no longer be the case for every situation.

Our view

A share sale has often been the default seller preference in Australia. The 50% CGT discount made the tax gap between a share sale and an asset sale followed by a franked dividend most often significant. Under indexation, that gap may compress, which make the analysis worthwhile.

Buyers have real commercial benefits from asset deals, including the potential step-up in depreciable assets and the removal of legacy liability exposure of the entity.

The facts are important, the nature of the assets, the depreciation position, the franking account balance, contract transfer and the liability profile of the business all bear on the outcome. No two situations are the same.

How Equion can support

Structure is one of the first decisions we work through with sellers, well before a process goes to market. A late change in deal structure is one of the most disruptive things that can happen in a transaction. Getting the question answered early costs nothing. Getting it wrong costs considerably more.

This document is prepared by Equion for general information purposes only and does not constitute legal, tax or financial advice. Based on publicly available Budget 2026–27 materials and subject to legislative change. All measures described are policy announcements only and have not yet been enacted. Recipients should obtain specific professional advice before making any decisions. © Equion 2026. All rights reserved. Confidential.